An¬†option is a¬†paper, that gives you a¬†right (not¬†duty) to¬†buy stocks (or¬†anything else) on¬†a¬†specific day. For¬†example, you bought an¬†option for¬†5$ which gives you the¬†right to¬†buy 1 share of¬†Apple in¬†one year for¬†todayвАЩs price of¬†150$. You expect Apple stocks to¬†rise by¬†more than 5$. LetвАЩs see 3 scenarios of¬†Apple price in¬†one year:

170$, we realize the option and get a profit of 170-150-5 = 15$. This is a 200% return. If we invested in a share, we would have got 170-150 = 20$ profit, 13%.

130$, we donвАЩt realize an¬†option, because now the¬†shares cost less, than in¬†the¬†contract (150$). We lose 5$ (the¬†cost of¬†an¬†option) instead of¬†130-150=-20$ if we bought a¬†share.

150$-155$, we may realize an option and get a small loss. 153-150-5=-2$. We lost 40$ instead of 2% profit.

If we had bought the shares, we would have risked losing all the share costs. Here we risk losing only the option price of 5$.

Options are the profit guarantee for a seller

A¬†seller wants to¬†have a¬†profit from a¬†share. Instead of¬†thinking about whether the¬†stock price will be as¬†high as¬†he wants or¬†not, he can just say: вАЬI want to¬†get 20$ profit in¬†one year from Apple shares that cost 150$, everything that is higher is yoursвАЭ. To¬†do so, he sells the¬†option for¬†20$. A¬†seller immediately gets a¬†profit of¬†20$ and¬†can invest then in¬†something else. Even if the¬†share price drops by¬†20$ to¬†130$, he does not¬†lose anything, as¬†well as¬†a¬†buyer.

Companies also issue options¬†вАУ Warrants. Companies give premiums to¬†employees as¬†an¬†option for¬†buying a¬†share of¬†a¬†company. For¬†example, Elon Musk gives Tesla employees options for¬†buying tesla at¬†a¬†huge discount, that they can realize at¬†any time. So that when employees save enough, they can invest money in¬†a¬†company. It is an¬†alternative to¬†convertible bonds.

European and American Options

European call (put)option is the right to buy(sell) a unit of an underlying asset at a strike (=pre-specified) price at a specific point in time.

American call (put)option is the right to buy(sell) a unit of an underlying asset at any time on or before an expiration date of an option. European options can also be without an expiration date.

American options are also traded in Europe, in the Netherlands stock exchange, Euronext.liffe, for example. These options are traded primarily on equities: FTSE-100, CAC40, Bel-20.

Price and problems with options

It is hard to estimate the price of an option. There are parameters, such as risk-free rate, time to expiration, and volatility (variance, or price fluctuation). For example, low-volatility options cost less over time, while high-volatility options cost a lot.

Formulas of option pricing

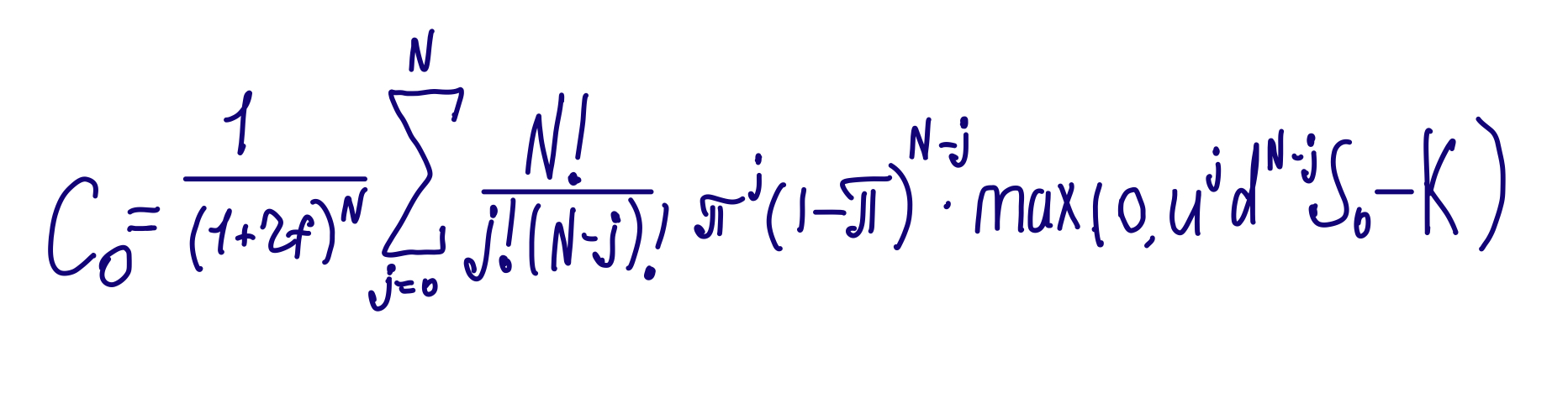

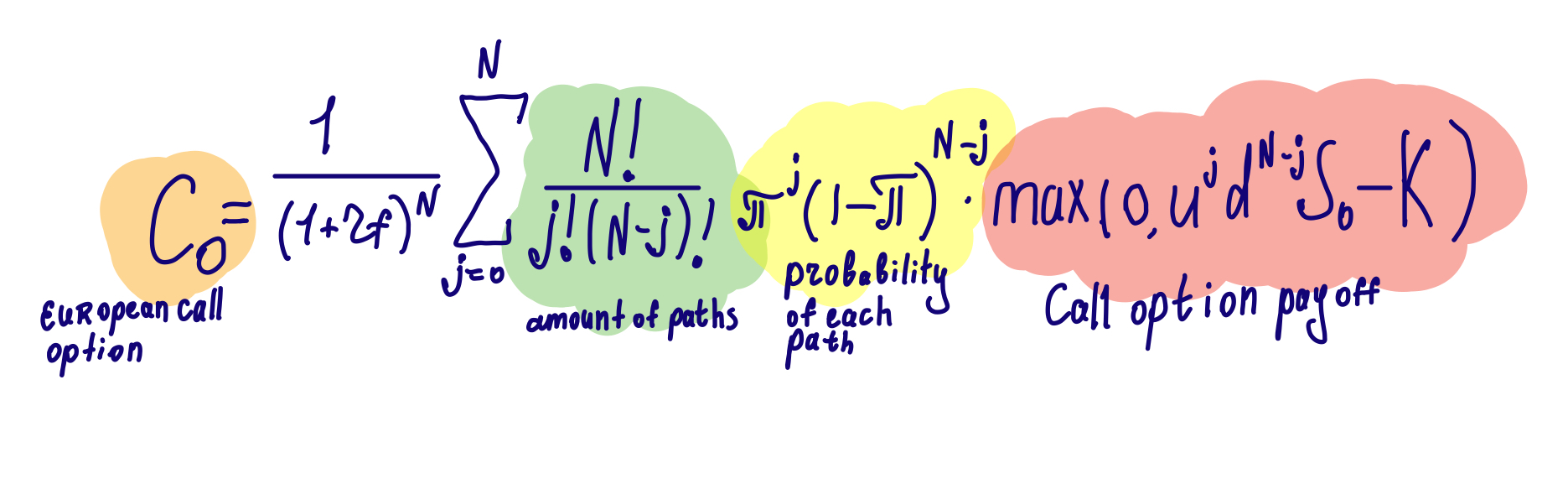

Binomial formula for pricing European options.

- K = strike price (end price, agreed before signing contract)

- N = periods of expiration

- S0 = current price of an asset

- rf = risk-free return per period

- ѕА= risk-neutral probability of¬†an¬†up move

- u = ratio of the share price to the prior share price, given that the upstate has occurred over a binomial step

- d = ratio of the share price to the prior share price, given that the downstate has occurred over a binomial step.

LetвАЩs understand each part of¬†the¬†equation:

The U and D are the possible outcomes (in $) of events. We assume, that there are always two scenarios in one period of time: positive and negative. Some traders use 1 second as a period, but then in 1 minute, there are 2^60, more than 1 billion scenarios. We assume 1 period as a quarter, half, or a full year.

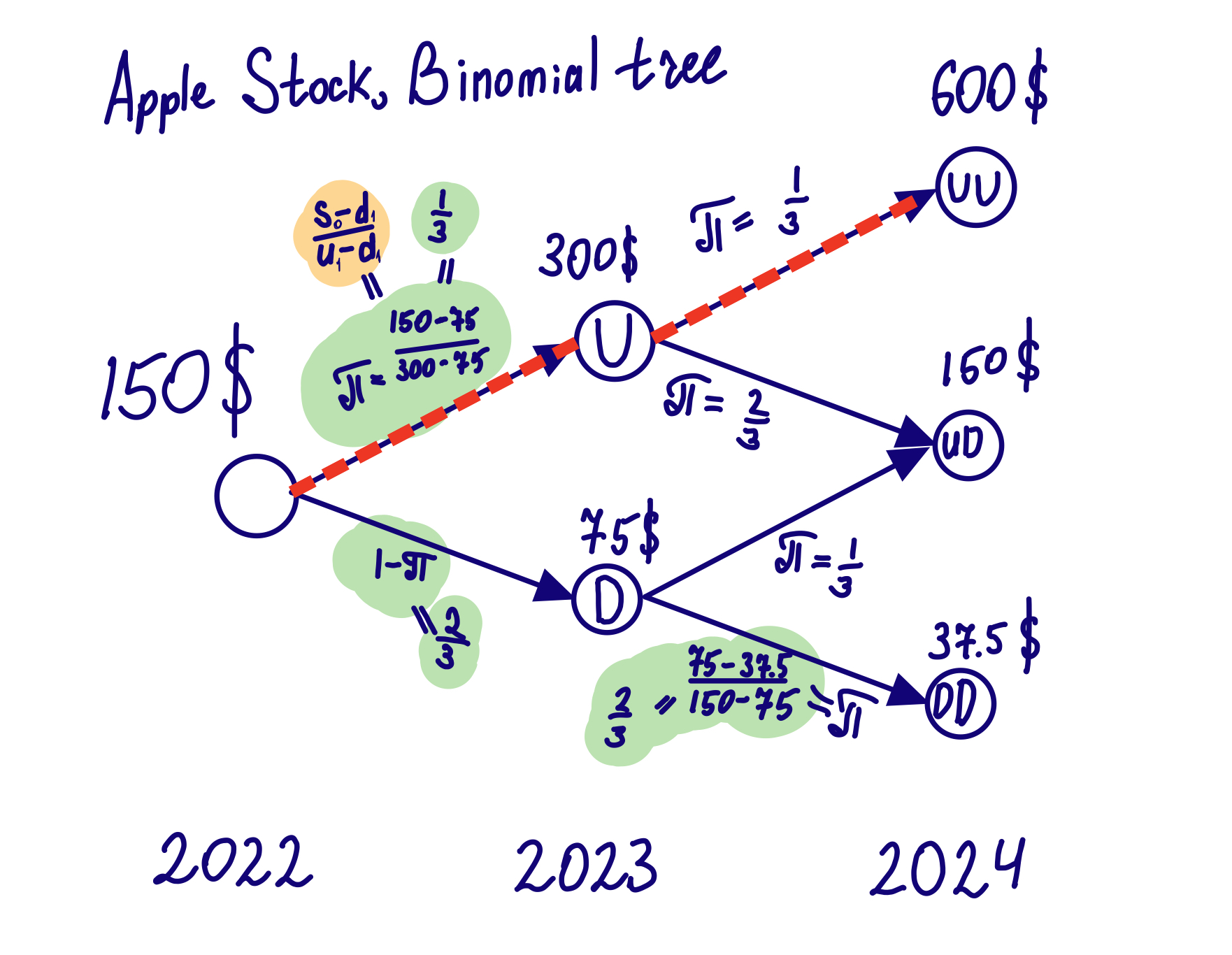

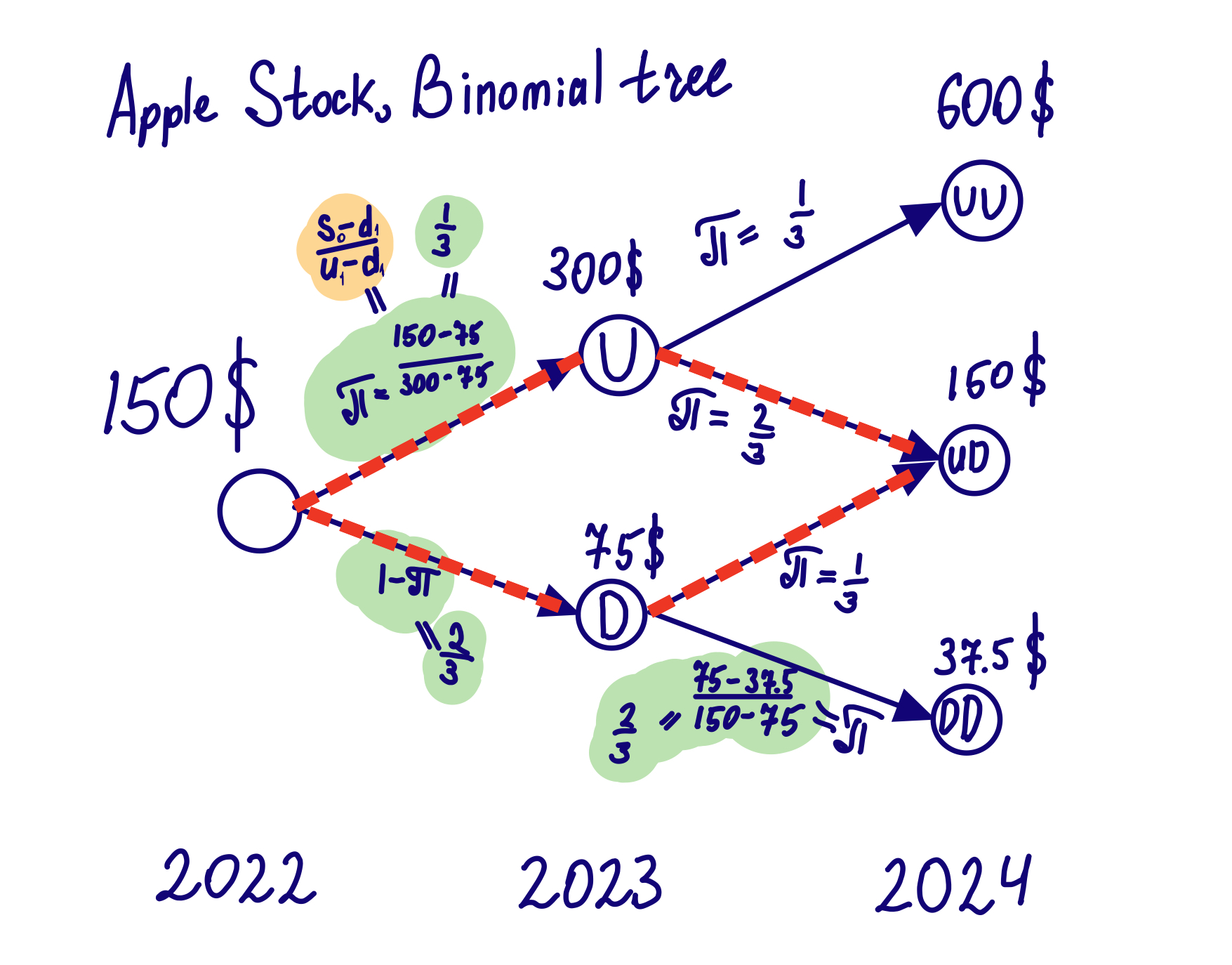

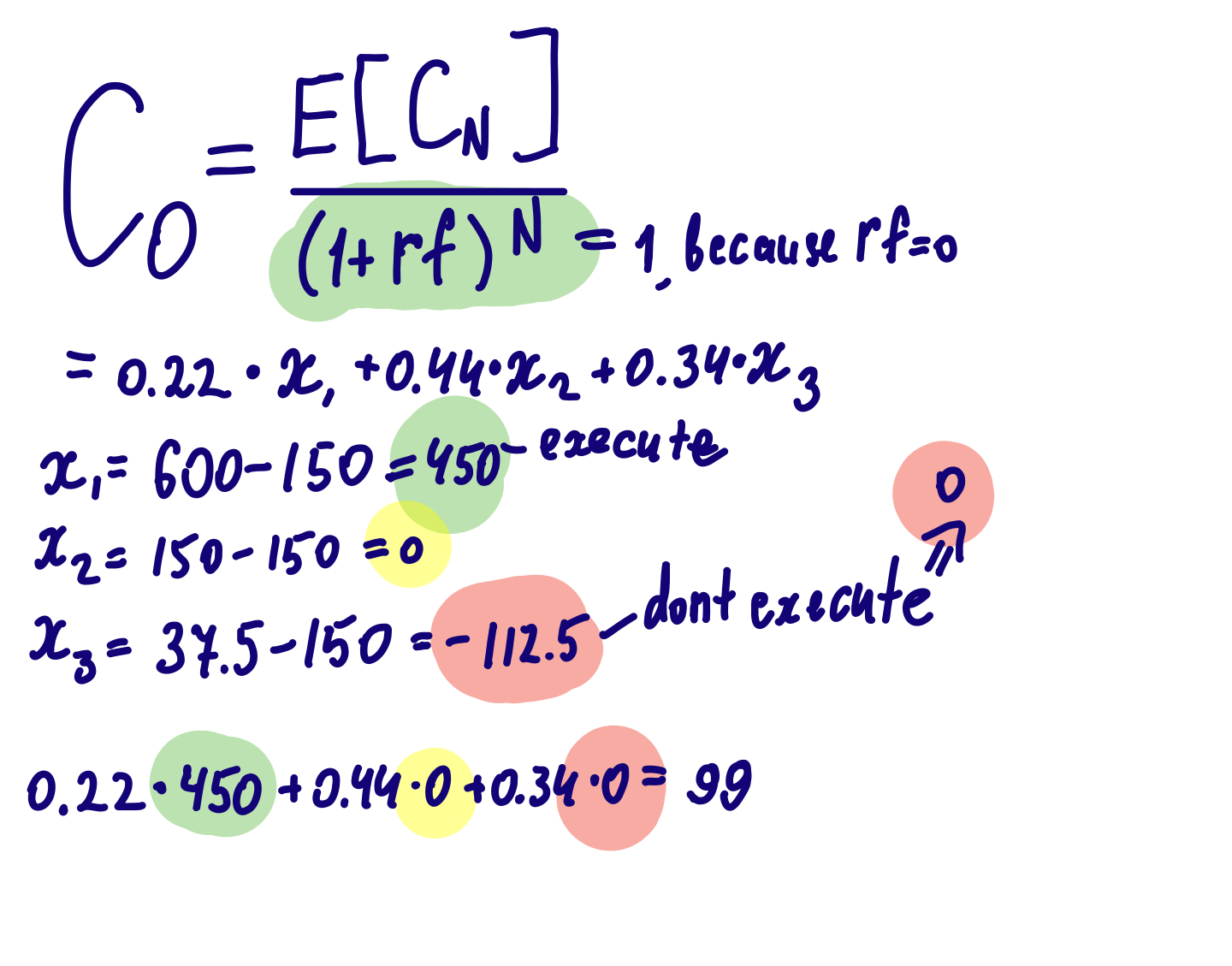

We put all possible outcomes in¬†a¬†binomial tree¬†вАУ a¬†graph, with 2 inherited sub-elements on¬†each node. LetвАЩs see the¬†binomial tree example of¬†Apple stock, which can either double or¬†halve, and¬†we also assume, that the¬†risk-free rate is equal to¬†0 for¬†simplicity:

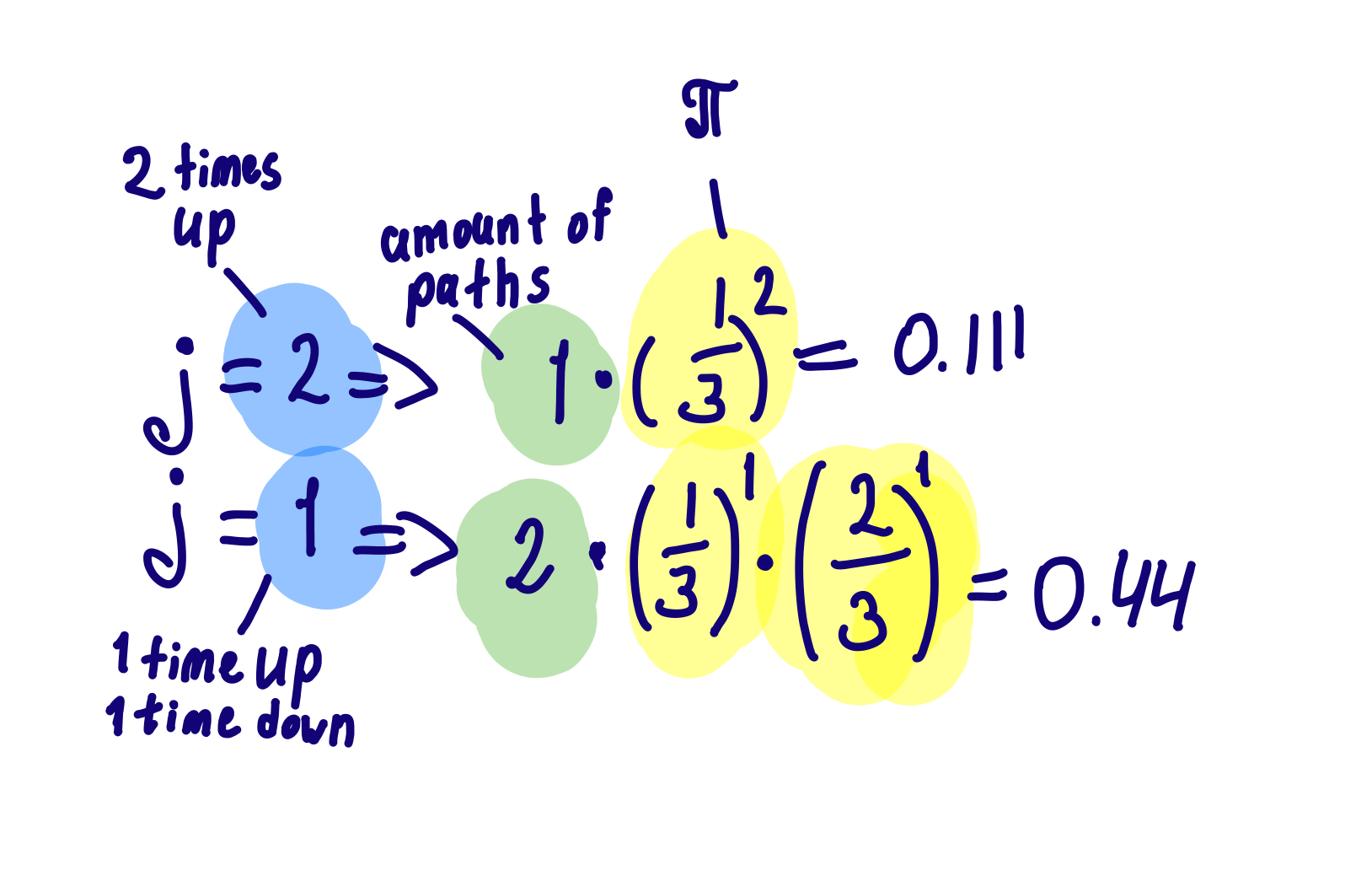

now we count the path to each final node:

It is 1 to UU, 2 to UD, and 1 to DD. Now we find the probability of each of the nodes.

The¬†probability of¬†the¬†last one is 1¬†вАУ 0.22¬†вАУ 0.44 = 0.34. Yes, the¬†probability of¬†the¬†nodes is neither 25% nor 33%, it is not¬†similarly distributed. It can only be similarly distributed if ѕА=0.5

Finally, we find the option price. We will assume that we need the strike price at the moment (ATM), that is equal to the spot value (S0):

The option price is equal to 99$.

Black Sholes Formula for American and European Options, with no-arbitrage:

- N = CDF of the normal distribution

- St = spot price of an asset (current price at time t)

- K = strike price (end price)

- rf = risk-free interest rate

- t = time to maturity

- ѕГ = volatility of¬†the¬†asset (variance)

arbitrage is a risk-free profit, that happens when tracking a portfolio (or a share) costs more (or less) than the derivative (forward or an option). If the share price is higher than the forward strike price (end-price) + the cost of a forward, then we short the share and buy a forward or an option.

That means if an Apple share costs 160$ and the forward cost is 0$, and the strike price is 150$, then we short apple stock and buy forwards. We get 160-150=10$ profit. Moreover, when we short a stock, we get the cost of a share to our account, that we can put in a bank. That brings a lot of profit.

LetвАЩs use an¬†option in¬†the¬†example above. LetвАЩs assume that an¬†option is free. We have the¬†same profit if the¬†cost of¬†apple stock is higher than 150$. If apple costs less than 150$, we just donвАЩt exercise the¬†option and¬†get profit from shorting a¬†stock. If the¬†cost of¬†an¬†option was 10$, then we just have a¬†profit of¬†160-150-5 + 160*(risk-free rate, such as¬†a¬†bank deposit).

As a result, we get risk-free profit from such operations. In a world with unlimited buyers and sellers, we could do the operation over and over again and become the richest people immediately, or in the end of a period.

Put-Call parity Price of a call (buy) and put (sell) options is different. that is because of a risk-free rate. We use an equation:

Call price - Put price = Current price - Present value of a Strike price

Call price - Put price = Current price - Strike price / (1 + risk-free rate)^periods

# usually, a period is equal to 1 year and is named "t"

C0 - P0 = S0 - K/(1 + rf)^t

Due to¬†the¬†always non-negative risk-free rate (because otherwise, you donвАЩt put money in¬†the¬†bank account), the¬†price of¬†a¬†call is higher than the¬†put.